Here is the complaint in R.J. Reynolds Tobacco Co. v. Dept. of Agriculture (D.D.C.):

News coverage here.

Here is the complaint in R.J. Reynolds Tobacco Co. v. Dept. of Agriculture (D.D.C.):

News coverage here.

Here (PDF).

An excerpt:

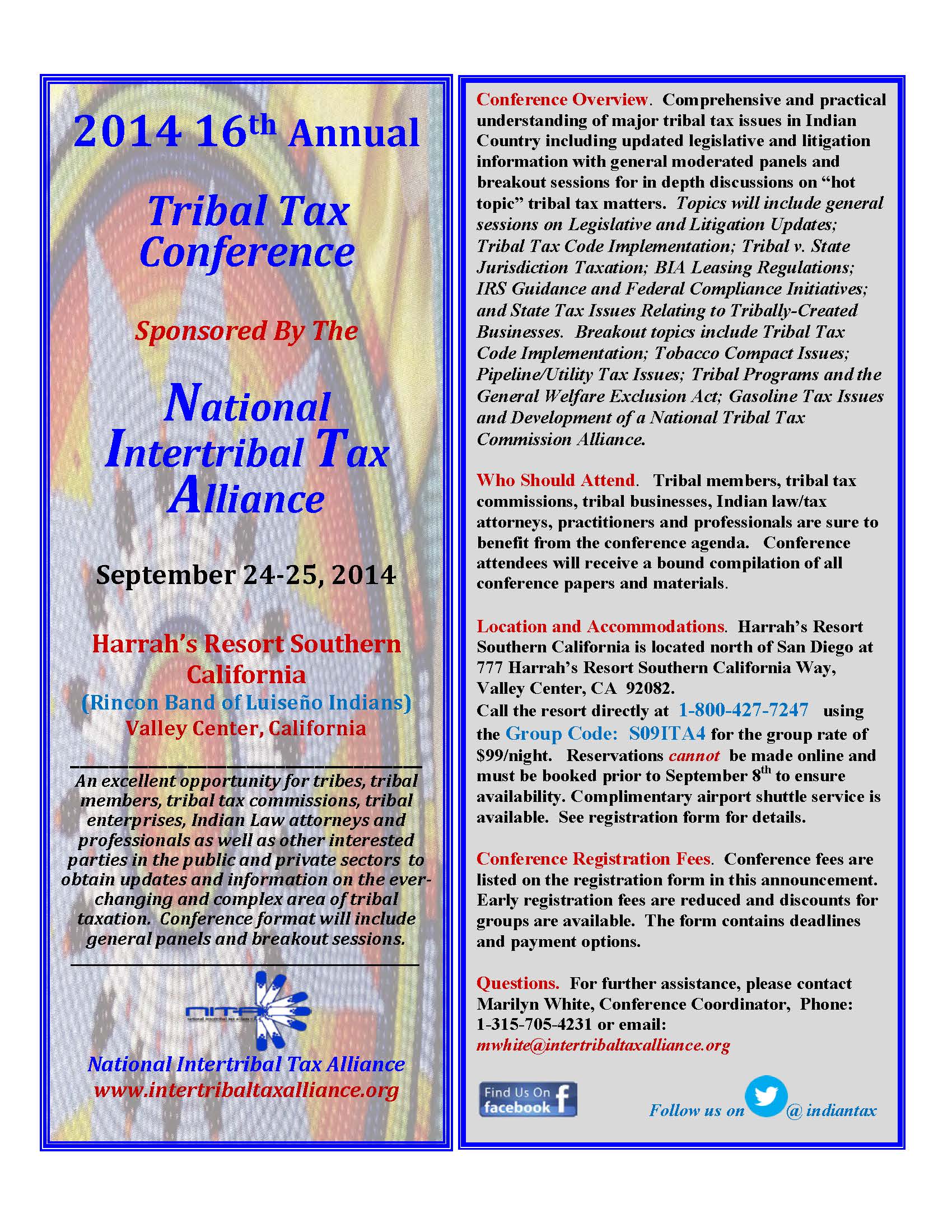

AKWESASNE, NY August 8, 2014— The National Intertribal Tax Alliance (NITA) announces its 16th Annual conference to be held September 24-25, 2014 at the Harrah’s Resort Southern California owned by the Rincon Band of Luiseño Indians. NITA is the foremost Native organization focusing on tribal taxation issues for tribal governments and tribal enterprises. NITA’s annual conferences attract many tribal tax commissioners, attorneys and other professionals interested in obtaining the latest updates on tribal tax issues.

The Rincon Band is pleased that the 16th Annual NITA Conference will be held at the newly-renovated Harrah’s Resort Southern California. Bo Mazzetti, Chairman of the Rincon Band, will deliver the welcoming address.

Headlining this year’s Conference is Keynote Speaker Matthew Fletcher, Professor of Law at Michigan State University College of Law and primary editor of the popular Indian law blog, “Turtle Talk.” (https://turtletalk.wordpress.com) This two-day conference includes general session panels and breakout sessions for more in-depth discussion on many complex tribal tax issues. General panels topics include Litigation and Legislative Updates; Tribal v. State Jurisdiction; BIA Leasing Regulations; IRS Guidance and Federal Compliance Initiatives; and State Tax Issues Relating to Tribal Businesses . Breakout session topics include Tribal Tax Code Implementation; Pipeline/Utility Tax Issues; Tribal Programs and the General Welfare Exclusion Act; Gasoline Tax Issues; and Development of a National Tribal Tax Commission Alliance.

NITA Chairperson Kelly Croman is extremely excited about this year’s conference emphasizing: “this year we have put together an ‘All-Star Cast’ of speakers and presenters for our conference.” “We expect a big turnout at the very popular and newly-renovated Harrah’s Resort and urge everyone who is interested to sign up early.”

Opinion here.

Applying § 15-35-102(11), MCA, to disallow a state tax deduction does not undermine the Tribe’s sovereign authority to tax or govern itself. The Legislature has simply chosen to limit the class of governments to which payment of taxes constitutes a deductible expense for coal producers. By so doing, the Legislature did not implicate tribal sovereignty.

Moreover, as the Department notes, WRI lacks standing to raise a claim implicating the Tribe’s sovereignty. See Northern Border Pipeline Co. v. State, 237 Mont. 117, 128-29, 772 P.2d 829, 835-36 (1989) (Taxpayer corporation had standing to challenge a state property tax, but did “not have standing to assert the Tribes’ sovereign right of self-government in doing so.”). The District Court did not err in so concluding.

Appellant’s Brief

Appellee’s Brief

Reply Brief

Here is in the Matter of Cougar Den Inc.:

In re Cougar Den 7-24-14 DOL decision

We posted on a similar matter here.

Five years ago, we at MSU conducted a study of what became an oral history of modern Michigan tribal-state relations under a contract with the National Congress of American Indians. Our former students did all the work — Alicia Ivory, Adrea Korthase, and Sheena Oxendine. For whatever reason, we never published the paper on our occasional paper website. The students interviewed many of the major players in tribal-state relations from the 2000s and before, including John Wernet, Jim Bransky, and Kathryn Tierney on the 2007 inland consent decree; Mike Petoskey and Kathryn Tierney on Michigan Court Rule 2.615; and Bill Brooks and John Wernet on the Michigan tribal-state tax agreements.

Here it is in its full glory, “Tribal-State Relations: Michigan as a Case Study”:

Here is the opening brief in Confederated Tribes and Bands of the Yakama Indian Nation v. Alcohol and Tobacco Tax and Trade Bureau:

Lower court materials in King Mountain Tobacco Co. v. Alcohol and Tobacco Tax and Trade Bureau (E.D. Wash.) are here.

Here are the materials in Blue Lake Rancheria v. Morgenstern (E.D. Cal.):

Blue Lake had prevailed in the Ninth Circuit before.

Here.

Here, NWS purposefully targeted the Oklahoma cigarette market and reaped the economic benefit of selling cigarettes in Oklahoma. Defiantly, NWS continued to import and distribute contraband Seneca cigarettes into Oklahoma and reap millions of dollars from the sale of the contraband cigarettes to Oklahoma consumers for more than two years after Oklahoma’s chief law enforcer filed this suit. NWS may not evade the public policy embodied in the MSA, the Escrow Statute, and the Complementary Act and thereby shift the burden of tobacco-related health care costs to the State. Disgorging gross receipts that NWS, a cigarette importer and distributor, received when it intentionally distributed contraband cigarettes into the Oklahoma market in violation of the Complementary Act is no more excessive than seizing and forfeiting contraband cigarettes from a cigarette distributer or wholesaler.22 NWS’ claim to Eighth Amendment protection minimizes the egregiousness of its flagrant disrespect for Oklahoma, our laws, and our citizens.

¶38 NWS had gross receipts that totaled at least $47,767,795.20 from the sale of contraband Seneca cigarettes for resale in Oklahoma from August of 2006 to August of 2010. Based upon the Complementary Act, the settled law of the case, and the undisputed material facts on summary judgment, the summary judgment was proper, and the district court did not abuse its discretion in denying NWS a new trial.

Here, with agenda, (PDF):

You must be logged in to post a comment.